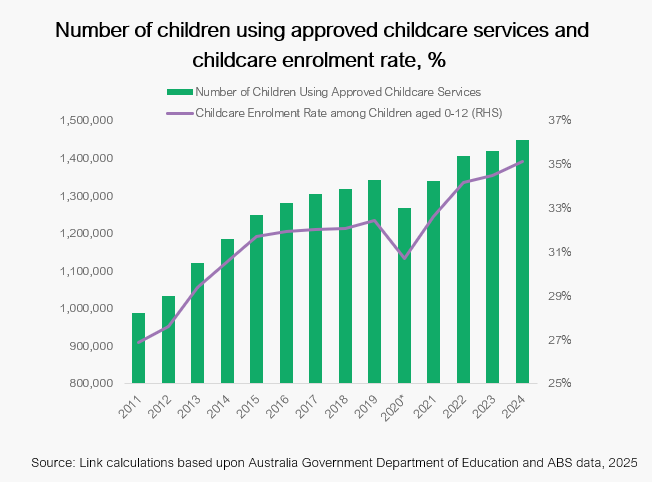

- Childcare enrolments have risen 22% over the past decade, reaching 1.4 million children in 2024. A key driver of rising childcare demand is Australia’s strong population growth supported by net overseas migration, much of which comprises of young adults in their prime child-rearing years. Also, rising female labour force participation is leading to more dual income households, which fuels a steady increase in childcare demand.

- Childcare subsidies reached A$14.8 billion in 2024, more than double that of a decade ago. The Child Care Subsidy (CCS) – Australia’s means-tested childcare system – limits out-of-pocket costs for many families to just ~10% of total fees, with the balance paid directly by the government to operators. The government is effectively underwriting operator revenues, making childcare real estate resemble a government-backed, inflation-protected bond.

- Furthermore, upcoming CCS reforms will guarantee three days of subsidised care per week for all families irrespective of their work status. As current enrolment rates of eligible children are not particularly high at only 35%, the policy reform should unlock significant new childcare demand. And this comes at a time when new childcare facility supply is constrained by high construction costs, stringent regulations, and a shortage in the number of childcare educators.

- Today, childcare property yields of ~5.4% offer a ~40 basis point premium to alternative real estate sectors such as purpose-built student accommodation (PBSA), exceeding the decade average premium. Growing institutional participation has improved the sector’s liquidity and exit optionality to local core capital. Investment volumes for Childcare real estate have exceeded PBSA on average since 2017. For non-core capital, forward-funding structures offer an attractive entry point in supply-constrained, high-demand urban locations. In our view, such assets are well-positioned to deliver strong risk-adjusted returns.

To request the full report, please reach out to us at LP@laml.com.