- U.S. Policy Headwinds: Aggressive U.S. tariffs on global imports, reminiscent of pre-World War 1, and a broader retreat from overseas markets, is fostering uncertainty that may depress U.S. growth and destabilize local financial markets. Such conditions are likely to impair U.S. real estate performance.

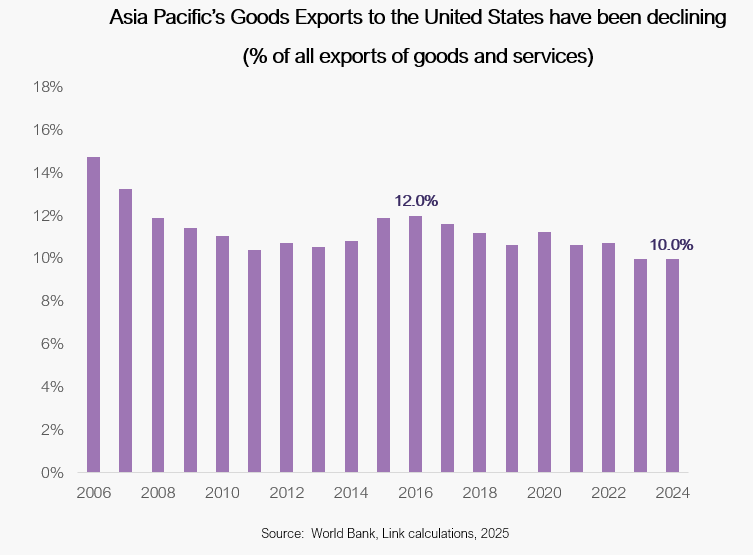

- Real Estate Allocation Shift: In light of these challenges, global real estate allocations to mature markets need to be reassessed. Diversification into Developed Asian markets (Japan, Australia, Singapore, South Korea, New Zealand and Hong Kong) which are characterized by low inflation, pro-growth economic policies, and enhanced intra-regional trade—can help mitigate exposure to the potential adverse effects of U.S. policy.

- Resilience Through Diversification: Developed Asian real estate offers an attractive diversification benefit. Historically, these markets have exhibited relatively higher returns, and a low correlation with U.S. and European assets, providing potential portfolio resilience during periods of market stress.

- Volatility presents Opportunity in Asia: Periods of market stress may present opportunities to acquire assets when liquidity is low, and sentiment is cautious. A decisive drop in interest rates, together with more powerful economic stimulus in China, would very likely mark a bottom in Asia’s real estate market. A strategic asset allocation to Developed Asia above the real estate market weight of 20% appears to be warranted.

To request the full report, please reach out to us at LP@laml.com.