- The multi-family rental sector has established its place firmly on the radar for institutional capital due to its relative stability amid significant economic volatility. Moreover, the sector has been a haven of stability amid structural demand shifts impacting offices and retail. Investors now face a further shifting of the landscape driven by growing backlash against immigration in North America and parts of Europe, with negative implications for demographics and housing demand.

- For institutional investors seeking opportunities with clear structural growth drivers, we view residential opportunities in Asia’s key developed market gateway cities as offering defensive market characteristics. Japan and Australia present distinct but complementary investment propositions that together represent the region’s most compelling multifamily allocation strategy.

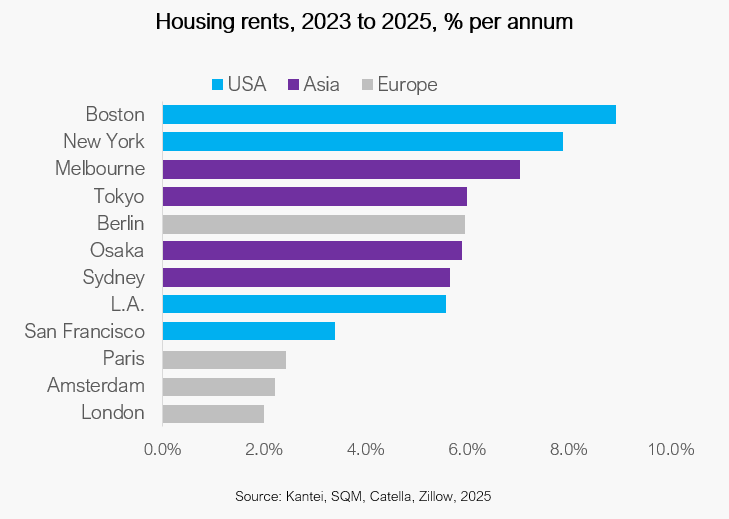

- Japan is emerging from decades of stagnation, with vacancies at 20-year lows and rents outpacing wages, offering a liquid, yield-driven market supported by proven demographic trends.

- Australia’s Build-to-Rent sector is a rare scale opportunity: only 0.4% of rental units are currently institutional-owned, while policy support and supply-demand imbalances create strong tailwinds.

- Both Japan and Australia benefit from political stability around immigration policies that drive sustained population growth in gateway cities without the social tensions plaguing Western nations. This demographic predictability, combined with compelling yield spreads, creates the foundation for strategic portfolio allocation.

To request the full report, please reach out to us at LP@laml.com.