- The Bank of Japan’s (BoJ) move to hike the policy rate to 1% should be read as confirmation that Japan has entered a reflationary economic cycle. Rates have risen, but policy remains accommodative relative to nominal GDP growth of around 4% per annum. Even if the policy rate rises further towards a likely peak of around 1.75%, monetary conditions would still be supportive by developed-market standards.

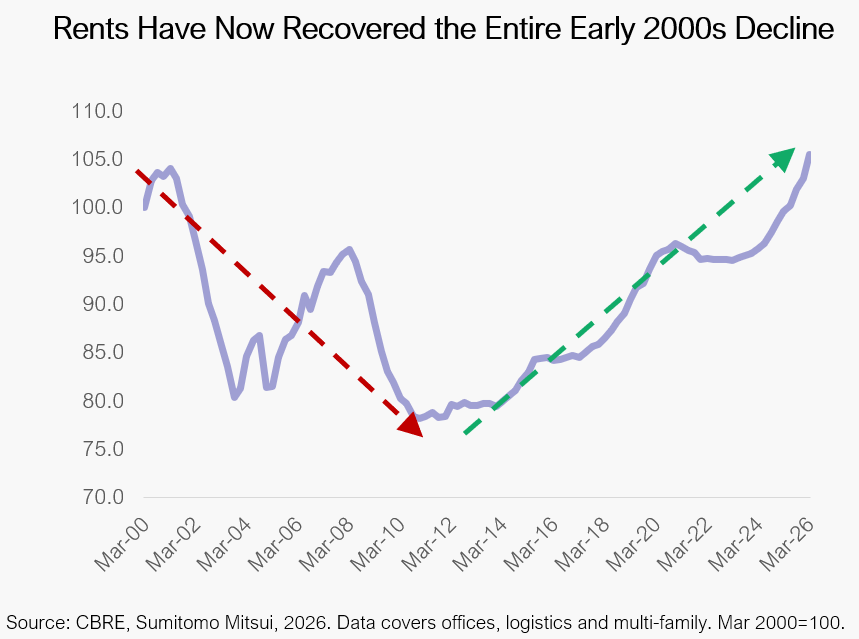

- The Japanese real estate investment market is no longer relying only on low interest rates. It is increasingly being supported by robust income growth. Tokyo Grade A office rents rose 15.5% YoY to Q1 2026, Osaka office rents rose 7.8%, and multifamily rents in Tokyo and Osaka are growing at around 4% YoY. That rental momentum is being reinforced by tight labour markets, urban population growth, and improving corporate profitability.

- Supply conditions make the rental growth story more durable. Across Tokyo and Osaka, 2026–28 completions are running below the 10-year average in major sectors, including multifamily, logistics and offices. At the same time, construction costs have risen materially faster than rents since 2022, making many new developments economically more marginal. For investors, this reduces the risk that new supply will dilute rent growth or undermine leasing assumptions.

- Yield spreads in Japan have compressed relative to risk-free rates and are now broadly comparable with Europe. However, Japan’s stronger rental momentum and more supportive policy backdrop provide a clearer fundamental justification for those spreads. The investment case is about buying income growth in a market where tenant demand is robust and supply is constrained.

- A value-add approach is the clearest way to translate this macro and rental-growth backdrop into portfolio returns and minimising downside risk to prices. Grade B office repositioning, hotel repositioning and corporate divestments all offer routes to acquire under-managed assets.

To request the full report, please reach out to us at [email protected].