- Following Labor's victory in the May 2025 election, which is the first time that the incumbent party has been re-elected in 21 years, Australia's real estate market remains fundamentally strong. Robust population growth underpins property demand with net migration in 2025 likely to again exceed pre-pandemic levels.

- Real estate rents across all sectors have on average grown 3.5% annually over the past decade, with 2024 showing 6% nominal growth. Supply constraints persist across most sectors with forecast completions in the next few years 30-40% below the decade average, supporting continued rent growth. Construction costs have escalated well ahead of capital values, by a margin of 20% since 2019, which is limiting new development. Logistics supply is elevated though also benefits from robust tenant demand.

- The RBA's monetary easing cycle is a positive for consumer spending as 80% of Australian mortgages are variable-rate, and higher consumption should offset headwinds from global trade tensions. Lower borrowing costs should also cement Australia’s position as one of the most favoured commercial real estate markets in Asia Pacific.

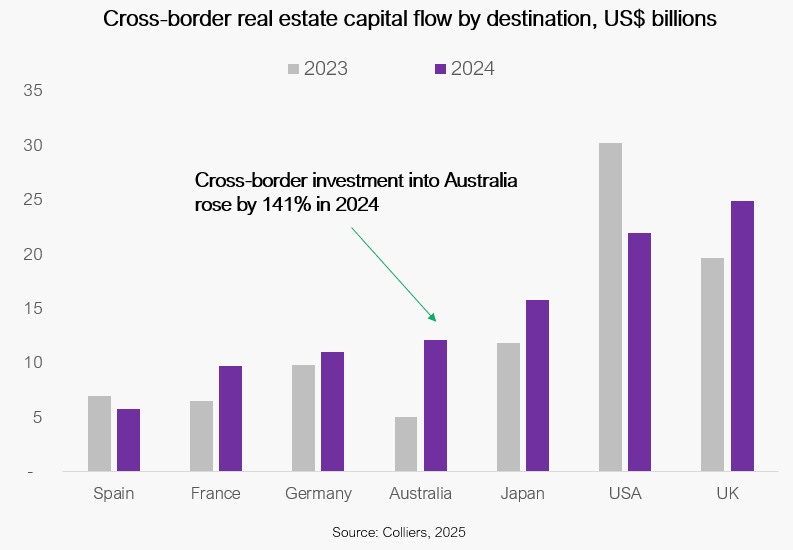

- The market globally recorded the fourth highest cross-border capital inflow in 2024, and is likely to remain favoured by international investors given its strong demographics. Amid ongoing global trade tensions, Australia is well placed to offer attractive risk-adjusted real estate returns in a global context.

To request the full report, please reach out to us at LP@laml.com.