- Three months into the Middle East war and the closure of the Strait of Hormuz, the central thesis of our March 2026 publication remains intact: the disruption is a pricing event for Asian real estate, not a structural reversal.

- Developed Asia’s economy has absorbed US$100-120/bbl. oil prices since the start of the war, supported by the powerful tailwind from global AI-related capex demand. Substantial strategic oil reserves have also cushioned the shock to Developed Asian economies, which has in turn helped sustain intra-regional activity.

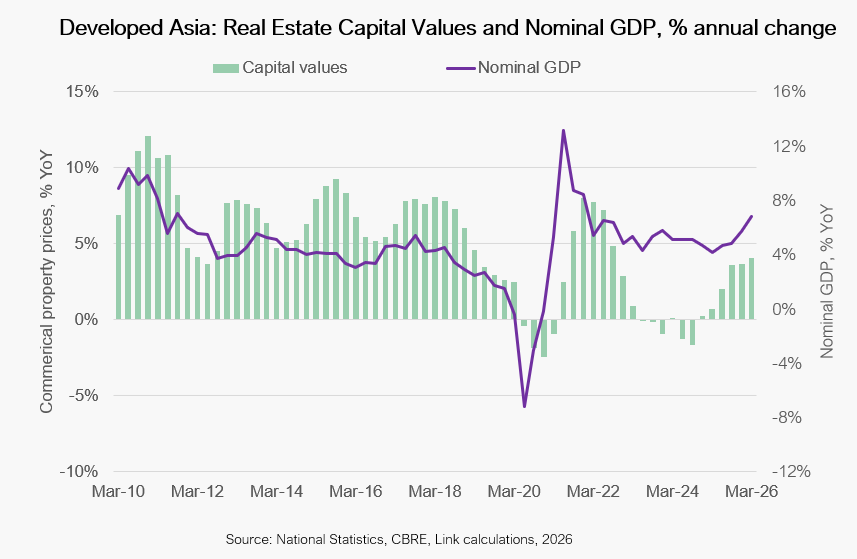

- Although significant uncertainty over the direction of the Middle East war exists, we frame the outlook around two judgement-based scenarios. In the base case, we assign a 70% weight to the Strait reopening by June; recent political negotiations point in this direction. In this case, Developed Asia real estate capital values could rise by 4–5% in 2026. Notably we expect Hong Kong to see the first broad-based rise in rents and capital values in five years.

- In the downside scenario, to which we assign a 30% weight, oil prices jump sharply to above US$150/bbl. during the summer before a resolution to the war occurs. The consequent economic growth pause leads to flat-to-negative capital values in 2026, followed by a rebound of 5% or more in 2027. We do not foresee a repeat of the 2022–23 rate-hiking cycle or a multi-year drop in values for Developed Asian real estate markets.

- Separately, we identify an unquantified tail risk that a political settlement does not emerge until the end of the year, and the Strait is effectively closed into 2027. In this case a growth pause risks becoming a recession. We do not assign formal probability to this outcome because geopolitical duration risk is unusually hard to judge. It is therefore treated as a stress case to monitor, not as a third formal scenario.

- The takeaway is to maintain Developed Asia allocations within a diversified global portfolio; treat current uncertainty as an opportunity for selective deployment; lean into the Hong Kong rebound where pricing is attractive.

To request the full report, please reach out to us at [email protected].