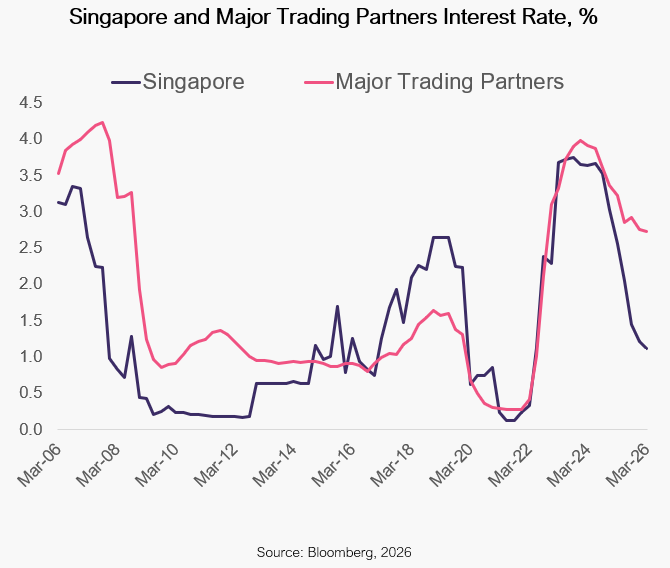

- The Monetary Authority of Singapore tightened monetary policy on 14th April. This is the first tightening since 2022, steepening the pace of Singapore dollar appreciation by an estimated 50 basis points to 1.0% per annum. Energy-related inflation triggered by the disruption of shipping in the Strait of Hormuz was the main reason for the policy tightening. Given Singapore’s near-total reliance on imports, it faces rapid and broad-based cost pass-through across its economy following a jump in oil and commodity prices.

- For the real estate sector, the decision carries a counterintuitive implication. Unlike most central banks, the MAS manages inflation through the exchange rate, not interest rates. Tightening means a stronger Singapore dollar, not necessarily higher borrowing costs. Singapore’s domestic rate (SORA) stands near 1%, among the lowest in the developed world. The combination of the MAS framework and Singapore’s safe-haven status means interest rates are unlikely to change materially soon.

- Against the background of low interest rates, we view the real estate sector as attractively positioned for selective investment. The rental cycle is turning higher amid limited new supply, and notwithstanding near-term headwinds from the energy-related disruption. The medium-term growth case is compelling; robust population growth, Singapore’s gateway role to ASEAN’s rapidly growing emerging markets, and direct exposure to the global AI investment cycle, all reinforce the positive growth outlook.

To request the full report, please reach out to us at LP@laml.com.